海外研报

筛选

GS--ECB—Cuts 25bp and Leaves Guidance Unchanged0005

BOTTOM LINE: The Governing Council cut policy rates by 25bp, as widely expected.

海外研报

2024年10月20日

FX Weekly--USD continues to rebound ahead of US election

FX View: The USD is on course to advance for the third consecutive week. We

海外研报

2024年10月20日

GS--Global Economics Wrap-Up: October 18, 2024

October central bank meetings in focus:

海外研报

2024年10月20日

UBS--Global forecasts001

CIO forecast tables reflect UBS CIO's view on growth, inflation, interest rates,

海外研报

2024年10月20日

GS--Diversify to Amplify | Carbonomics

From a top-down perspective, Peter Oppenheimer notes while the macro outlook

海外研报

2024年10月20日

UBS--High yield CIO View: High yield

We have a Neutral recommendation on high yield. We believe total

海外研报

2024年10月20日

UBS--Limited surprise and focus on long-term direction

More policies to attract talent: The Hong Kong

海外研报

2024年10月20日

Jefferies - Chris Wood - Alternative narratives and Trump rising_20241017

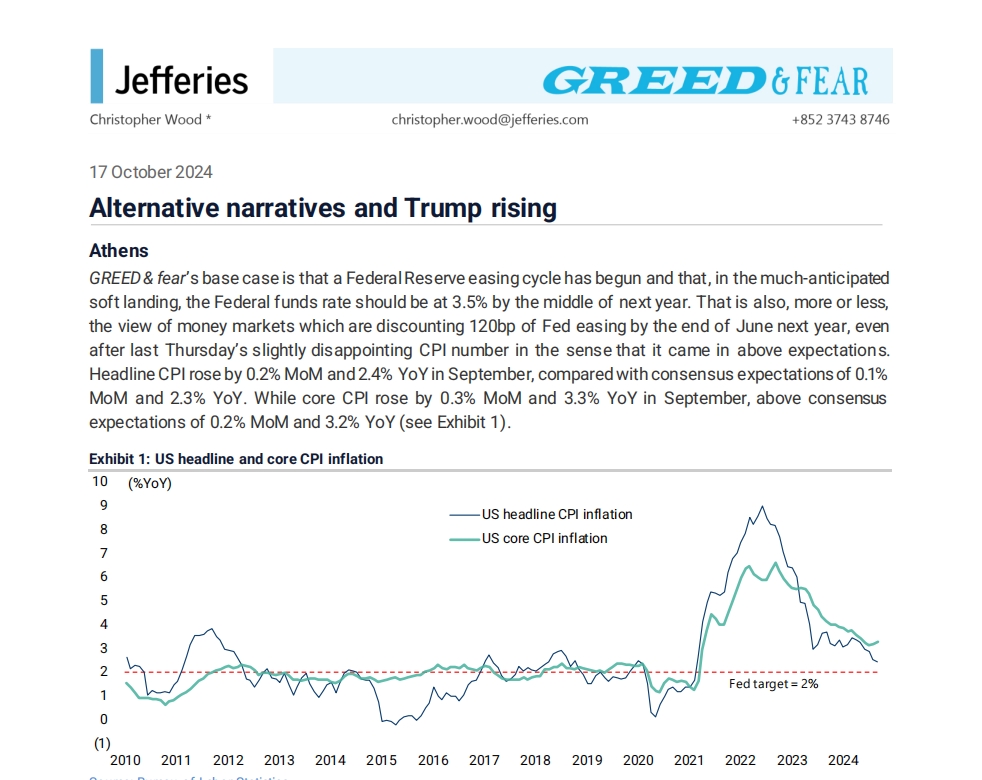

GREED & fear’s base case is that a Federal Reserve easing cycle has begun and that, in the

海外研报

2024年10月20日